Normality Tests and Outliers#

Introduction#

In many statistical analyses, we assume that the data we are analyzing follows a normal distribution. This assumption is important because many statistical tests are based on the assumption of normality. However, in reality, data often does not follow a normal distribution perfectly. Therefore, it is important to test the normality of our data before we conduct any statistical analyses.

Variability of Gaussian samples#

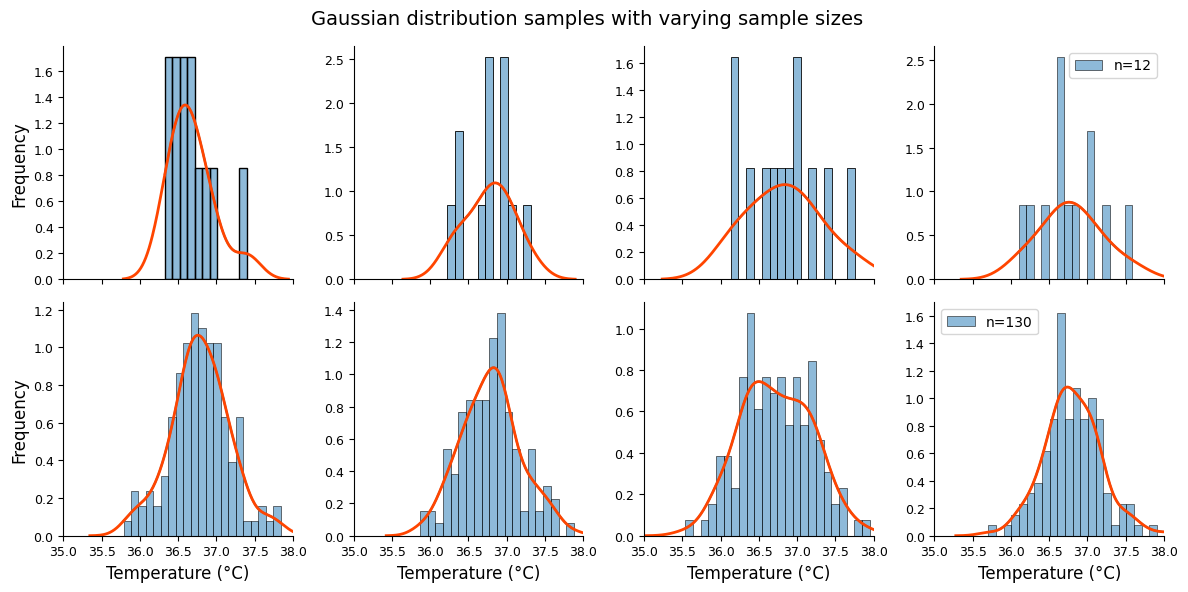

The figure below illustrates the reality of Gaussian distributions in practice. Even when values are randomly drawn from a perfect bell curve (with identical mean and standard deviation), the resulting samples rarely look perfectly symmetrical. This is especially noticeable in small samples (top graphs, n=12) compared to larger ones (bottom graphs, n=130).

import numpy as np

import matplotlib.pyplot as plt

import seaborn as sns # for easy KDE plotting

np.random.seed(111)

# Sampling parameters

mean_temp = 36.8

std_temp = 0.4

sample_sizes = [12, 130]

num_cols = 4

# Pre-generate random values (for efficiency)

random_samples = {

size: np.random.normal(

loc=mean_temp, scale=std_temp, size=(num_cols, size))

for size in sample_sizes

}

# Create subplots and share x-axis for consistent scaling

fig, axes = plt.subplots(

nrows=len(sample_sizes),

ncols=num_cols,

figsize=(12, 6),

sharex=True,

)

# Main title for the entire figure

fig.suptitle(

"Gaussian distribution samples with varying sample sizes",

fontsize=14)

for row, size in enumerate(sample_sizes):

for col in range(num_cols):

ax = axes[row, col] # Get the current subplot

sns.histplot( # Use seaborn for histogram with KDE

random_samples[size][col],

stat="density",

binwidth=0.1,

kde=True,

ax=ax,

label=f"n={size}",

)

# Plot the KDE separately with desired color and linewidth

sns.kdeplot(

random_samples[size][col],

ax=ax,

color='orangered',

linewidth=2

)

ax.set_xlabel('Temperature (°C)')

# Only label the y-axis for the first plot in each row

ax.set_ylabel('Frequency' if col == 0 else "")

# Add legend only to the last plot in each row

if col == num_cols-1:

ax.legend()

plt.xlim((35, 38))

sns.despine()

plt.subplots_adjust(top=0.9) # Adjust to avoid title overlap

plt.tight_layout();

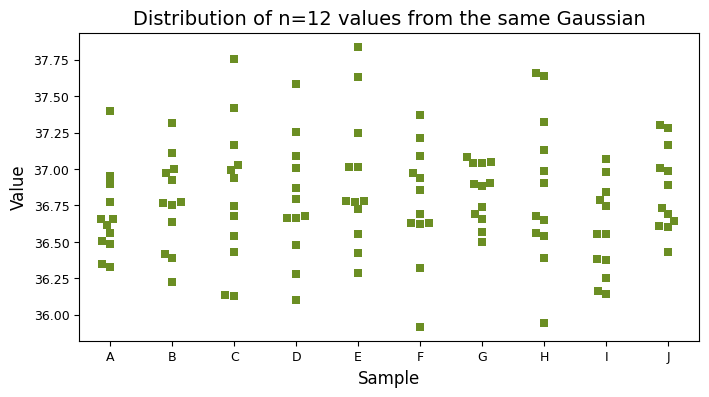

Even though all samples are drawn from the same theoretical distribution, they exhibit natural variation due to random sampling. The swarm plot below vividly demonstrates this, showing how each sample can differ slightly in its shape and spread.

np.random.seed(111)

# Parameters

mean_temp = 36.8

std_temp = 0.4

labels = list("ABCDEFGHIJ") # Cleaner way to create a list of labels

sample_size = 12

# Generate and reshape data

data = np.random.normal(

loc=mean_temp,

scale=std_temp,

size=len(labels) * sample_size)

data = data.reshape((len(labels), sample_size))

# Create a list of sample labels for each data point

sample_labels = np.repeat(labels, sample_size) # Repeat each label 12 times

# Flatten the data array

flattened_data = data.flatten()

# Create a dictionary for seaborn's data format

data_dict = {

'Sample': sample_labels,

'Value': flattened_data}

# Plot using seaborn with the dictionary data format

plt.figure(figsize=(8, 4))

sns.swarmplot(

x='Sample', y='Value', data=data_dict,

color="olivedrab",

marker='s',

size=6)

plt.title(

"Distribution of n=12 values from the same Gaussian",);

Assessing the normality of data#

The assumption of normality underpins many statistical procedures. But how can we determine whether our data truly follow a Gaussian distribution? Fortunately, we have an arsenal of tools at our disposal, both graphical and statistical, to assess normality.

Graphical methods provide a visual first impression, helping us identify obvious departures from normality. Statistical tests, on the other hand, offer a more rigorous quantitative assessment.

Q-Q plots#

One of the most powerful tools for visual assessment is the quantile-quantile (Q-Q) plot. This plot compares the quantiles of the observed data against the quantiles of a theoretical normal distribution. If the data is perfectly normal, the points on the Q-Q plot will fall along a straight diagonal line. Deviations from this line signal departures from normality. How a Q-Q Plot is Constructed:

Percentiles: the Q-Q plot begins by calculating the percentile rank of each value in the dataset. This tells us the proportion of values that are smaller than or equal to a given value.

Theoretical quantiles (Z-Scores): for each of these percentiles, the plot determines the corresponding Z-score in a standard normal distribution (mean = 0, standard deviation = 1). This Z-score indicates how many standard deviations away from the mean we would need to go in a normal distribution to reach that same percentile.

Predicted values: using the actual mean and standard deviation calculated from the dataset, the plot converts these theoretical Z-scores into predicted values. These are the values we would expect to see at each percentile if the data were perfectly normally distributed.

Plotting: finally, the Q-Q plot displays the observed data values on the y-axis and the corresponding predicted values (based on a normal distribution) on the x-axis.

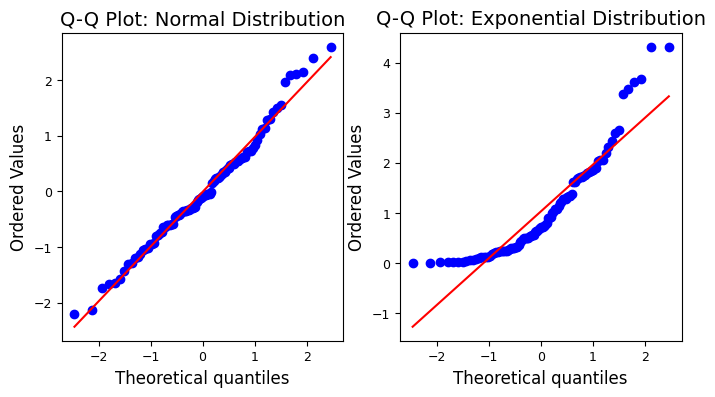

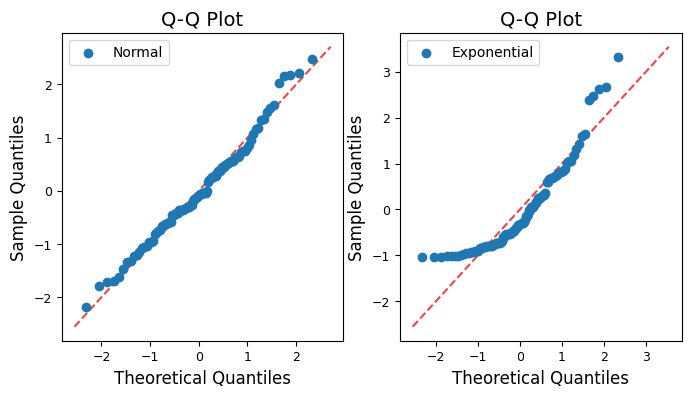

Q-Q plots with scipy: normal vs. exponential#

Let’s use scipy.stats.probplot to create Q-Q plots that visually assess the normality of data sampled from normal and exponential distributions.

import scipy.stats as st

np.random.seed(111)

# Sample Generation (more descriptive variable names)

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

# Plotting (using a loop for conciseness and consistency)

fig, axes = plt.subplots(1, 2, figsize=(8, 4))

titles = [

"Q-Q Plot: Normal Distribution",

"Q-Q Plot: Exponential Distribution",

]

for i, (data, title) in enumerate(zip([normal_data, exponential_data], titles)):

st.probplot(data, plot=axes[i])

axes[i].set_title(title);

The Q-Q plot for the normally distributed sample closely follows a straight line, indicating normality, while the plot for the exponentially distributed sample deviates significantly from the straight line, revealing its non-normal nature.

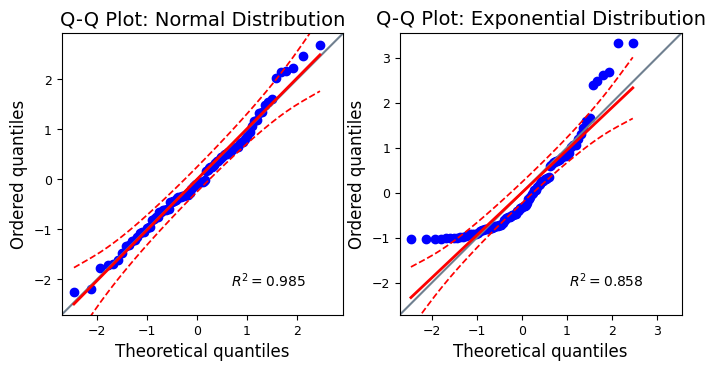

Q-Q plot with pingouin#

The pingouin library in Python offers a convenient function called qqplot for creating Q-Q plots. It simplifies the process and provides additional features, such as confidence intervals and customizable distributions for comparison. Of note, pingouin.qqplot uses a simulation-based approach to calculate confidence intervals, making it more robust for smaller sample sizes.

import pingouin as pg

np.random.seed(111) # For reproducibility

# Sample Generation

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

# Plotting

fig, axes = plt.subplots(1, 2, figsize=(8, 4))

titles = [

"Q-Q Plot: Normal Distribution",

"Q-Q Plot: Exponential Distribution",

]

for i, (data, title) in enumerate(zip([normal_data, exponential_data], titles)):

pg.qqplot(

data,

dist='norm', # compare the data against the normal distribution

ax=axes[i],

confidence=0.95, # Add 95% confidence intervals

)

axes[i].set_title(title);

The confidence intervals show the range within which we would expect the sample quantiles to fall if the data were truly drawn from a normal distribution. If most of the points in the Q-Q plot fall within the confidence intervals, it provides evidence in favor of the normality assumption. Points falling outside the confidence intervals suggest deviations from normality and warrant further investigation.

Alternative options for ploting Q-Q plots#

Besides scipy.stats and pingouin, there are several other Python packages we can use to create Q-Q plots or similar visualizations for assessing normality:

statsmodels.graphics.gofplots.qqplot: a flexible function for creating Q-Q plots, offering customization options like different line types (e.g., standardized, theoretical quantiles, regression line) and marker styles. We can also add a fitted line for better visual comparison.sklearn.preprocessing.QuantileTransformer: this transformer isn’t specifically designed for Q-Q plots, but we can use it creatively. By transforming the data to a normal distribution and comparing the original and transformed quantiles, we essentially create a Q-Q plot-like visualization.Manual Q-Q Plot with

matplotlib: if we want complete control over the plot’s appearance, we can create a Q-Q plot manually using Matplotlib. This involves calculating the theoretical and sample quantiles oursleves and then plotting them as a scatter plot, as shown below.

from scipy.stats import norm

def qq_plot(data, ax=None, **kwargs):

"""Creates a Q-Q plot using Matplotlib.

Args:

data (array-like): The data to plot.

ax (matplotlib.axes.Axes, optional): The axes to plot on. If None,

a new figure and axes will be created.

**kwargs: Additional keyword arguments passed to ax.scatter.

Returns:

matplotlib.axes.Axes: The axes object on which the plot was drawn.

"""

if ax is None:

fig, ax = plt.subplots()

# Sort the data

data_sorted = np.sort(data)

# Theoretical quantiles

theoretical_quantiles = norm.ppf(np.linspace(0, 1, len(data)))

# Scatter plot of sample quantiles vs. theoretical quantiles

ax.scatter(

theoretical_quantiles,

data_sorted,

**kwargs

)

# Add diagonal line

lims = [

np.min([ax.get_xlim(), ax.get_ylim()]),

np.max([ax.get_xlim(), ax.get_ylim()])

]

ax.plot(

lims, lims,

'r--', alpha=0.75, zorder=0,

)

# Labels and title

ax.set_xlabel("Theoretical Quantiles")

ax.set_ylabel("Sample Quantiles")

ax.set_title("Q-Q Plot")

ax.legend()

return ax

# Example Usage

np.random.seed(111)

# Standardize both datasets

normal_data_std = (normal_data - np.mean(normal_data)) / np.std(normal_data)

exponential_data_std = (exponential_data - np.mean(exponential_data)) / np.std(exponential_data)

fig, axes = plt.subplots(1, 2, figsize=(8, 4))

qq_plot(

normal_data_std,

ax=axes[0],

label='Normal')

qq_plot(

exponential_data_std,

ax=axes[1],

label='Exponential');

Initially, i.e., without standardisation, the Q-Q plot for the exponential distribution does appear shifted upwards compared to the theoretical normal quantiles, as shown elsewhere. The exponential distribution is right-skewed, meaning it has a long tail on the right side and most of its values are concentrated on the left side, while the normal distribution is symmetrical, with values evenly distributed around the mean.

When we create a Q-Q plot with the exponential distribution against the normal distribution, we’re essentially comparing two distributions with very different shapes. This leads to the observed pattern:

Lower quantiles: the lower quantiles of the exponential distribution (values on the left side) will be smaller than the corresponding quantiles of a normal distribution. This causes the points on the Q-Q plot to fall below the diagonal line in the lower left corner.

Upper quantiles: the upper quantiles of the exponential distribution (values on the right side) will be larger than the corresponding quantiles of a normal distribution. This pushes the points on the Q-Q plot above the diagonal line in the upper right corner, creating the appearance of an upward shift.

pingouin.qqplot scales the y-axis of the Q-Q plot according to the theoretical quantiles of the specified distribution (dist). When dist=’norm’, the y-axis is scaled to the standard normal distribution (mean=0, std=1). For non-normal distributions like the exponential, the scaling of the y-axis might not align perfectly with the range of the observed data, leading to a visual shift. One way to address this is to standardize both the normal and exponential data before creating the Q-Q plots. This ensures that both datasets have a mean of 0 and a standard deviation of 1, making the comparison more visually accurate.

Statistical tests for normality#

To complement these visual assessments, statistical tests offer a more objective and quantitative way to evaluate whether the data significantly deviates from a normal distribution.

Statistical normality tests operate by comparing the observed data to what would be expected under a perfect normal distribution. They then quantify the discrepancy between the two, typically resulting in a test statistic and a P-value.

Test statistic: this is a numerical measure of how far the data deviates from the expected pattern of a normal distribution. Larger test statistic values generally indicate a greater departure from normality.

P-value: the P-value tells us the probability of observing a test statistic as extreme as or more extreme than the one we calculated, assuming that the data is truly normal. A small P-value (typically less than 0.05) suggests that the data is unlikely to have come from a normal distribution, leading to the rejection of the null hypothesis of normality. A large P-value (typically greater than 0.05) suggests that the observed deviations from normality could be due to chance, and we fail to reject the null hypothesis of normality.

In the following subsections, we’ll dive into three commonly used statistical tests for normality:

D’Agostino-Pearson omnibus K² normality test: a versatile test that assesses both skewness (asymmetry) and kurtosis (tailedness) of the data to determine if it deviates from normality.

Shapiro-Wilk test: often considered the most powerful test for small to medium sample sizes, it focuses on how closely the data matches the expected order statistics of a normal distribution.

Kolmogorov-Smirnov test: a more general test that can compare the data to any theoretical distribution, not just the normal. While less powerful than the Shapiro-Wilk test for normality, it offers greater flexibility.

D’Agostino-Pearson omnibus K² normality test#

The D’Agostino-Pearson omnibus K-squared test is a versatile and powerful statistical test designed to assess whether a dataset deviates significantly from a normal distribution. Unlike some other tests that focus on a single aspect of normality, the omnibus K² test examines both skewness and kurtosis, providing a more comprehensive evaluation.

Skewness and Kurtosis#

Skewness measures the asymmetry of a distribution. A normal distribution is perfectly symmetrical (skewness = 0). Positive skewness indicates a long right tail, while negative skewness indicates a long left tail.

Kurtosis measures the “tailedness” or “peakedness” of a distribution relative to a normal distribution. A normal distribution has a kurtosis of 3. A higher kurtosis (leptokurtic) implies heavier tails and a sharper peak, while a lower kurtosis (platykurtic) suggests lighter tails and a flatter peak.

It’s calculated as the “fourth standardized moment of the distribution”: \(\text{kurtosis} = E[(X - \mu)^4 / \sigma^4]\), with \(E\) the expected value (average), \(X\) a random variable, \(\mu\) the mean of the distribution, and \(\sigma\) the standard deviation of the distribution. For a normal distribution, when we calculate this fourth standardized moment, it turns out to be exactly 3.

np.random.seed(111) # For reproducibility

# Sample Generation

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

# Calculate and print results

print("Distribution\tSkewness\tKurtosis")

print("-" * 40) # Adding a separator for visual clarity

print(f"Normal\t\t{st.skew(normal_data):.3f}\t\t\

{st.kurtosis(normal_data, fisher=True):.3f}")

print(f"Exponential\t{st.skew(exponential_data):.3f}\t\t\

{st.kurtosis(exponential_data, fisher=True):.3f}")

# by subtracting 3, the Fisher definition establishes a baseline of zero for a normal distribution

Distribution Skewness Kurtosis

----------------------------------------

Normal 0.354 0.167

Exponential 1.374 1.654

# Calculate descriptive statistics using `describe`

print("Normal samples:")

print("Skewness = ", st.describe(normal_data).skewness)

print("Kurtosis = ", st.describe(normal_data).kurtosis)

Normal samples:

Skewness = 0.35440679809917

Kurtosis = 0.1665451056955929

The skewness of the normal data is close to 0 (indicating symmetry) and the excess kurtosis is close to 0 (indicating tailedness similar to a normal distribution). These values are consistent with the expectation for normally distributed data. In contrast, the skewness of exponential data is positive (around 2), indicating a long right tail. The excess kurtosis is also positive (around 2), showing heavier tails than a normal distribution. These values confirm the non-normal, skewed nature of exponential data.

How the K² test works#

Sample statistics: the test first calculates the sample skewness and kurtosis from the data.

Z-scores: these skewness and kurtosis values are then transformed into Z-scores. These Z-scores indicate how many standard deviations each value deviates from the expected value under normality (0 for skewness and 3 for kurtosis).

Fisher’s Z-score transformation: the Z-score transformation for kurtosis specifically accounts for the fact that a normal distribution has a Fisher kurtosis of 0. It is calculated by subtracting 3 from the Pearson kurtosis. This transformation ensures that a normally distributed sample would have a kurtosis Z-score close to 0.

K² statistic: the Z-scores for skewness and kurtosis are squared and summed to form the omnibus K-squared statistic.

P-value: the K² statistic is approximately chi-square distributed with 2 degrees of freedom under the null hypothesis of normality. This allows us to calculate a P-value, which represents the probability of observing a K² statistic as extreme as or more extreme than the one calculated from the data, assuming normality holds true.

A small p-value (typically less than 0.05) indicates that the observed skewness and/or kurtosis are significantly different from what would be expected in a normal distribution, providing evidence against the normality assumption.

A large p-value suggests that the data are consistent with normality (i.e., we fail to reject the null hypothesis).

Manual implementation of the K² test#

We can implement the D’Agostino-Pearson test from scratch using NumPy and SciPy functions. This involves calculating skewness and kurtosis, transforming them into Z-scores, and then computing the K2 statistic and its associated p-value using the chi-square distribution.

from scipy.stats import skew, kurtosis, chi2

def dagostino_pearson_test(data):

"""Performs the D'Agostino-Pearson omnibus K2 test for normality.

Args:

data (array-like): The data to test for normality.

Returns:

statistic: The K2 test statistic.

p_value: The p-value for the hypothesis test.

"""

n = len(data)

if n < 8:

raise ValueError("Sample size must be at least 8 for the test.")

# Calculate sample skewness and kurtosis (Fisher's definition)

s = skew(data)

k = kurtosis(data, fisher=True)

# Calculate intermediate terms

y = s * np.sqrt((n + 1) * (n + 3) / (6 * (n - 2)))

beta_two = (

(3 * (n**2 + 27*n - 70) * (n + 1) * (n + 3))

/

((n - 2) * (n + 5) * (n + 7) * (n + 9))

)

w_two = -1 + np.sqrt(2 * (beta_two - 1))

delta = 1 / np.sqrt(np.log(np.sqrt(w_two)))

alpha = np.sqrt(2 / (w_two - 1))

# Calculate Z-scores

z_skew = delta * np.log(y / alpha + np.sqrt((y / alpha)**2 + 1))

z_kurt = (k / (2 * np.sqrt(3 * (n - 1) / ((n + 1) * (n + 3)))))

# Calculate K2 statistic

k2 = z_skew**2 + z_kurt**2

# Calculate p-value using chi-square distribution with 2 degrees of freedom

p_value = 1 - chi2.cdf(k2, 2)

return k2, p_value

# Example usage with consistent seed

np.random.seed(111) # Same seed for both samples

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

for data, sample_type in zip([normal_data, exponential_data], ["Normal", "Exponential"]):

k2, pval = dagostino_pearson_test(data)

print(f"{sample_type:<12} D'Agostino-Pearson K²={k2:.2f} p-value={pval:.3f}")

Normal D'Agostino-Pearson K²=2.50 p-value=0.286

Exponential D'Agostino-Pearson K²=46.43 p-value=0.000

K² test with scipy.stats.normaltest#

The D’Agostino-Pearson omnibus K² test is a powerful normality test that assesses both skewness and kurtosis, suitable for various sample sizes, but it may be less sensitive to deviations in the distribution’s center and overly sensitive to outliers in small samples. Let’s demonstrate the scipy.stats.normaltest function in action to assess normality concretely.

np.random.seed(111)

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

# Function to perform the test and print results

def test_and_print(data, sample_type):

k2, pval = st.normaltest(data)

print(f"{sample_type:<12} D'Agostino-Pearson K²={k2:.2f} P-value={pval:.3f}")

# Perform tests and print results (using the function)

print("\n--- D'Agostino-Pearson Omnibus K² Test ---")

test_and_print(normal_data, "Normal:")

test_and_print(exponential_data, "Exponential:")

--- D'Agostino-Pearson Omnibus K² Test ---

Normal: D'Agostino-Pearson K²=2.70 P-value=0.259

Exponential: D'Agostino-Pearson K²=29.04 P-value=0.000

The P-value for the normal data is high (0.259), indicating we fail to reject the null hypothesis of normality. This is consistent with the data being sampled from a normal distribution. In contrast, the P-value for the exponential data is very small (0.000), indicating we strongly reject the null hypothesis of normality. This is expected, as exponential data is not normally distributed.

Note: Minor differences in results between the manual D’Agostino-Pearson implementation and scipy.stats.normaltest are likely due to floating-point arithmetic and rounding errors inherent in numerical calculations, implementation details such as optimizations or approximations used in scipy.stats, as well as software versions and potential updates to the algorithms in scipy.stats. Don’t overinterpret small variations, especially if both lead to the same conclusion about normality. Focus on practical significance and, if uncertain, use additional tests to confirm the findings. We can generally trust scipy.stats.normaltest as it’s well-maintained and widely used, but the manual implementation is a valuable learning exercise and cross-check ;-)

Shapiro-Wilk test#

The Shapiro-Wilk test stands out as a powerful and widely used statistical test for assessing normality, particularly for small to moderate sample sizes (up to 5000 data points). The study from Razali and Wah (2011) demonstrated its slightly superior power compared to other normality tests, making it a preferred choice in many scenarios.

How the Shapiro-Wilk test works#

At its core, the Shapiro-Wilk test compares the observed distribution of the data to an idealized normal distribution. Here’s a simplified breakdown:

Sorting: the test starts by sorting the data points from smallest to largest.

Expected values: it then calculates the values we would expect to see at each rank (percentile) if the data were perfectly normally distributed. These expected values are based on the properties of the standard normal distribution (mean = 0, standard deviation = 1).

Correlation: the test assesses the correlation between the observed sorted values and their corresponding expected values. If the data is perfectly normal, this correlation should be very high.

Test statistic (W): the correlation is transformed into a test statistic called \(W\), which ranges from 0 to 1. Values closer to 1 indicate a better fit to normality.

P-value: finally, a P-value is calculated based on the W statistic. A small P-value (typically < 0.05) suggests that the observed data are unlikely to have come from a normal distribution, leading to the rejection of the null hypothesis of normality.

While modern algorithms extend the Shapiro-Wilk test’s applicability to 5000 data points, it’s still not ideal for very large samples. For samples exceeding this limit, consider alternative tests like the D’Agostino-Pearson omnibus K2 test. Another limitation is that the Shapiro-Wilk test is generally powerful, but it might not be the most sensitive to specific types of deviations from normality, such as those affecting only the tails of the distribution.

Application of scipy.stats.shapiro#

Let’s demonstrate how to apply the Shapiro-Wilk test in Python using the scipy.stats module, in particular the shapiro function and interpret its results to gain deeper insights into the normality of the data.

np.random.seed(111) # for reproducibility

# Sample Generation

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

# Function to perform the Shapiro-Wilk test and print results

def shapiro_wilk_test(data, sample_type):

statistic, p_value = st.shapiro(data)

print(f"{sample_type:<12} Shapiro-Wilk W = {statistic:.3f}, P-value = {p_value:.3f}")

# print(f"{' ':<15} {'(Reject H0 if p < 0.05)':>30}") # H0: Data is normal

# Perform Shapiro-Wilk test and print results

print("\n--- Shapiro-Wilk Test ---")

shapiro_wilk_test(normal_data, "Normal:")

shapiro_wilk_test(exponential_data, "Exponential:")

--- Shapiro-Wilk Test ---

Normal: Shapiro-Wilk W = 0.984, P-value = 0.263

Exponential: Shapiro-Wilk W = 0.855, P-value = 0.000

The W statistic for the normal data (0.984) is close to 1, indicating a good fit to normality. Combined with the high P-value, this strongly supports the hypothesis that the data is normally distributed. In contrast, the W statistic for the exponential data (0.855) is lower, suggesting a less good fit to normality. Along with the extremely low P-value, this provides strong evidence against the normality of the exponential data.

Normality tests using pingouin#

Pingouin’s normality function actually performs both the Shapiro-Wilk test and the D’Agostino-Pearson test. We can easily access the results for either test from the returned dataframe.

import pingouin as pg

np.random.seed(111) # For reproducibility

# Sample Generation

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

# Function to perform tests and print results

def normality_tests(data, sample_type):

print("\n--- Normality Tests for", sample_type, "---")

print(f"{'Test':<20} {'W':<8} {'P-value':<6}")

# Shapiro-Wilk Test

shapiro_results = pg.normality(data, method='shapiro')

print(f"{'Shapiro-Wilk':<20} {shapiro_results['W'][0]:<8.3f} \

{shapiro_results['pval'][0]:<6.3f}")

# D'Agostino-Pearson Test

dagostino_results = pg.normality(data, method='normaltest')

print(f"{'D\'Agostino-Pearson':<20} {dagostino_results['W'][0]:<8.3f} \

{dagostino_results['pval'][0]:<6.3f}")

print("-" * 40)

# Perform tests and print results

normality_tests(normal_data, "Normal Data")

normality_tests(exponential_data, "Exponential Data")

--- Normality Tests for Normal Data ---

Test W P-value

Shapiro-Wilk 0.984 0.263

D'Agostino-Pearson 2.703 0.259

----------------------------------------

--- Normality Tests for Exponential Data ---

Test W P-value

Shapiro-Wilk 0.855 0.000

D'Agostino-Pearson 29.044 0.000

----------------------------------------

Omnibus test for normality using statsmodels#

The omni_normtest function offers a convenient way to assess normality in the data. The term “omnibus” means “including or covering many things.” In the context of normality testing, an omnibus test combines multiple aspects of normality into a single test statistic. The omni_normtest function in statsmodels does this by evaluating both skewness and kurtosis, similar to the D’Agostino-Pearson test, by incorporating three different tests, i.e., the Jarque-Bera test, the skewness test and the kurtosis test.

The function calculates the test statistics for each of the three individual tests, and then combines the P-values from these individual tests using Fisher’s method to obtain an overall omnibus test statistic (chi-square distributed). Finally, the test calculates a single P-value based on this omnibus test statistic. This P-value indicates the overall probability of observing the combined test results if the data were truly normally distributed.

import statsmodels.api as sm

np.random.seed(111) # For reproducibility

# Sample Generation

normal_data = np.random.normal(size=100)

exponential_data = np.random.exponential(size=100)

# Function to perform the omnibus test and print results

def omnibus_normality_test(data, sample_type):

omnibus_stat, omnibus_pvalue = sm.stats.stattools.omni_normtest(data)

print(f"\n--- Omnibus Normality Test for {sample_type} ---")

print(f"Omnibus Statistic: {omnibus_stat:.3f}")

print(f"Omnibus p-value: {omnibus_pvalue:.3f}")

# print(f"{'(Reject H0 if p < 0.05)':>30}") # H0: Data is normal

# Perform tests and print results

omnibus_normality_test(normal_data, "Normal Data")

omnibus_normality_test(exponential_data, "Exponential Data")

--- Omnibus Normality Test for Normal Data ---

Omnibus Statistic: 2.703

Omnibus p-value: 0.259

--- Omnibus Normality Test for Exponential Data ---

Omnibus Statistic: 29.044

Omnibus p-value: 0.000

It’s important to note that the omni_normtest function is not the most powerful test for normality, especially for smaller sample sizes. For smaller samples, the Shapiro-Wilk test is often preferred. Moreover, the omnibus nature of this test makes it difficult to pinpoint exactly which aspect of normality (skewness or kurtosis) is being violated if the null hypothesis is rejected.

Kolmogorov-Smirnov test#

The Kolmogorov-Smirnov (K-S) test is a versatile nonparametric test used to assess whether two samples are drawn from the same distribution or whether a single sample follows a specified theoretical distribution. Unlike parametric tests like the t-test, which primarily focus on differences in location (means), the K-S test is sensitive to differences in both location, scale (spread), and shape, making it a more comprehensive tool for comparing distributions.

The K-S test comes in two flavors:

One-Sample K-S test: compares the empirical distribution function (ECDF) of the observed data to the cumulative distribution function (CDF) of a reference distribution (e.g., normal, exponential, uniform). This helps us determine if the sample data likely comes from the specified distribution.

Two-Sample K-S test: compares the ECDFs of two independent samples to assess whether they are likely drawn from the same underlying distribution, even if that distribution is unknown.

The core idea behind the K-S test is simple yet powerful: it quantifies the maximum vertical distance (absolute difference) between the two cumulative distribution functions being compared. This maximum distance is the K-S test statistic, often denoted as \(D\). A larger K-S statistic indicates a greater discrepancy between the two distributions, providing stronger evidence against the null hypothesis of identical distributions.

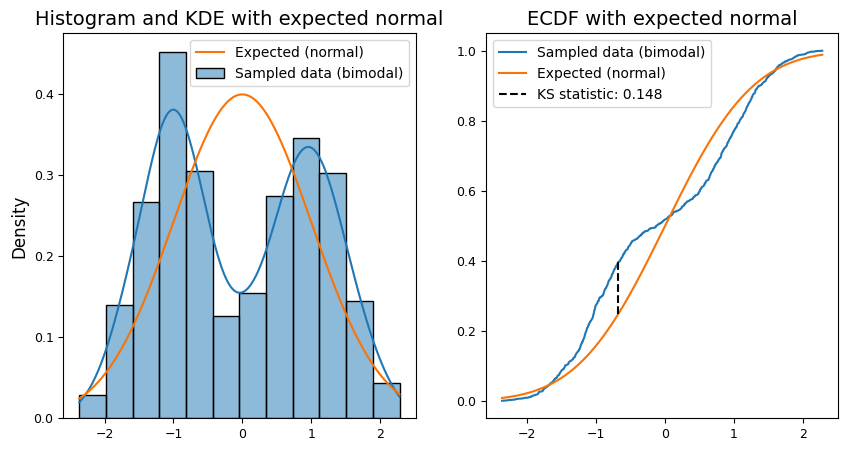

np.random.seed(111) # for reproducibility

# Sample Generation (bimodal distribution)

sample_size = 1000

sample = (

np.random.randn(sample_size)

* 0.5

+ 1

- 2 * (np.random.random(sample_size) > 0.5)

)

# ECDF Function

def ecdf(data):

"""Compute ECDF for a one-dimensional array of values."""

x = np.sort(data)

y = np.arange(1, len(data) + 1) / len(data)

return x, y

# Calculate ECDFs

sample_x, sample_ecdf = ecdf(sample)

normal_cdf = norm.cdf(sample_x)

# KS Statistic

ks_stat = np.max(np.abs(normal_cdf - sample_ecdf))

# Plotting

fig, axes = plt.subplots(1, 2, figsize=(10, 5))

# Histogram and KDE Plot

sns.histplot(

sample,

label="Sampled data (bimodal)",

stat="density",

kde=True,

ax=axes[0],

)

sns.lineplot(

x=sample_x,

y=norm.pdf(sample_x),

color="xkcd:orange",

label="Expected (normal)",

ax=axes[0],

)

axes[0].set_title(

"Histogram and KDE with expected normal",)

axes[0].legend()

# ECDF Plot

sns.lineplot(

x=sample_x,

y=sample_ecdf,

label="Sampled data (bimodal)",

ax=axes[1],

)

sns.lineplot(

x=sample_x,

y=normal_cdf,

color="xkcd:orange",

label="Expected (normal)",

ax=axes[1],

)

# Highlight the max difference (KS statistic)

max_diff_idx = np.argmax(

np.abs(normal_cdf - sample_ecdf)

)

axes[1].vlines(

x=sample_x[max_diff_idx],

ymin=min(sample_ecdf[max_diff_idx], normal_cdf[max_diff_idx]),

ymax=max(sample_ecdf[max_diff_idx], normal_cdf[max_diff_idx]),

colors="black",

linestyles="dashed",

label=f"KS statistic: {ks_stat:.3f}"

)

axes[1].set_title(

"ECDF with expected normal",)

axes[1].legend();

We can perform the (one-sample) K-S test using scipy.stats.kstest as shown below.

The test statistic (D) measures the maximum absolute difference between the empirical cumulative distribution function (ECDF) of the sample and the cumulative distribution function (CDF) of the standard normal distribution. A larger D value suggests a greater discrepancy from normality. In addition, the P-value is the probability of observing a test statistic as extreme as or more extreme than the calculated D, assuming the null hypothesis (normality) is true. A small p-value (typically < 0.05) provides evidence against normality.

np.random.seed(111) # For reproducibility

# Sample Generation (bimodal distribution)

sample_size = 1000

sample = np.random.randn(sample_size) * 0.5 + 1 - 2 * (np.random.random(sample_size) > 0.5)

# Perform the one-sample Kolmogorov-Smirnov test

ks_statistic, p_value = st.kstest(

sample,

'norm', # 'norm' specifies the normal distribution

)

# Output the results with clear formatting

print("\n--- One-Sample Kolmogorov-Smirnov Test ---")

print(f"Null Hypothesis (H0): sample comes from a normal distribution")

print(f"Test statistic (D): {ks_statistic:.3f}")

print(f"P-value: {p_value:.5f}")

if p_value < 0.05: # Typical significance level

print("Reject H0: evidence suggests the sample is NOT normally distributed")

else:

print("Fail to reject H0: insufficient evidence to conclude the sample \

is not normally distributed")

--- One-Sample Kolmogorov-Smirnov Test ---

Null Hypothesis (H0): sample comes from a normal distribution

Test statistic (D): 0.148

P-value: 0.00000

Reject H0: evidence suggests the sample is NOT normally distributed

Given that the sample is intentionally generated as a bimodal distribution, we expect the P-value to be very small, indicating strong evidence against the null hypothesis of normality. This would align with the visual inspection of the ECDF plots, where the sample distribution clearly deviates from the normal curve.

The K-S test finds applications in various fields:

Goodness-of-fit testing: assessing whether data fits a particular theoretical distribution (e.g., testing for normality).

Comparing sample distributions: determining if two groups differ significantly in their underlying distributions.

Model validation: evaluating the fit of statistical models by comparing the predicted and observed distributions.

Quality control: testing the uniformity of random number generators.

Additional normality tests#

In addition to the D’Agostino-Pearson, Shapiro-Wilk, and Kolmogorov-Smirnov tests, several other statistical tests can assess normality:

Anderson-Darling test: a modification of the Kolmogorov-Smirnov test that is often more powerful, particularly for detecting deviations in the tails. (Available in

scipy.stats.anderson).Lilliefors test: a corrected version of the Kolmogorov-Smirnov test that is more appropriate when the population parameters are unknown. (Available in

statsmodels.stats.diagnotic.lilliefors).Jarque-Bera test: similar to D’Agostino-Pearson, but less powerful, especially for small samples. Often used in econometrics. (Available in

scipy.stats.jarque_bera).Shapiro-Francia test: a computationally lighter alternative to Shapiro-Wilk for large samples (typically > 50). (Available in the

sfranciapackage).Cramér-von Mises test: measures the overall difference between the observed and theoretical distributions. (Available in

scipy.stats.cramervonmisesfunction).

Choosing a Test:

Shapiro-Wilk is a good general-purpose test.

Shapiro-Francia or Anderson-Darling are suitable for large samples.

Shapiro-Wilk is better for small samples.

Anderson-Darling is sensitive to tail deviations.

Lilliefors is suitable when parameters are unknown.

Jarque-Bera is often used in time series and econometrics.

Combining visual inspection with multiple tests is recommended for a well-rounded assessment of normality.

Outliers#

An outlier is a data point that significantly deviates from the overall pattern of the dataset, raising questions about its origin and validity. It’s a value so extreme that it appears to belong to a different population than the rest of the data. Outliers can arise from various sources, both benign and problematic:

Data entry errors: typos, miscalculations, or incorrect measurements can easily introduce outliers. Or it can be a missing value encoded as ‘999’.

Biological diversity: in biological data, outliers can reflect genuine natural variation. Some individuals simply fall at the extreme ends of a trait’s distribution.

Random chance: even in perfectly controlled experiments, statistical fluctuations can occasionally produce extreme values.

Experimental mistakes: equipment malfunctions, protocol deviations, or contamination can lead to erroneous data points.

Invalid assumptions: sometimes, what appears to be an outlier under one statistical model might fit perfectly under a different model. For example, data that seems like an outlier in a normal distribution might be entirely expected in a lognormal distribution.

Graphical approaches for outlier detection#

General-purpose outlier detection methods#

For effectively detecting outliers in the data, we may combine both graphical and statistical methods. First of all, we need to understand the data:

Contextual knowledge: leverage the domain expertise to define what constitutes an “outlier” in the context of the specific data and research question. Is it an extreme value, an unexpected pattern, or something else?

Data exploration: conduct a thorough exploratory data analysis (EDA) to understand the central tendency, spread, and overall shape of the data. This will help identify reasonable ranges and establish a baseline for outlier detection.

Visual inspection can be achieved using different tools:

Univariate data:

Histograms: looking for isolated bars or gaps in the distribution.

Box plots: identifying points that fall outside the whiskers (\(1.5 \times \text{IQR}\) from the quartiles).

Normal Q-Q plots: checking if points deviate significantly from the diagonal line, especially in the tails.

Multivariate data:

Scatter plots: visualizing relationships between pairs of variables and look for isolated points.

Scatterplot matrices: examining multiple pairwise relationships simultaneously to spot outliers across different dimensions.

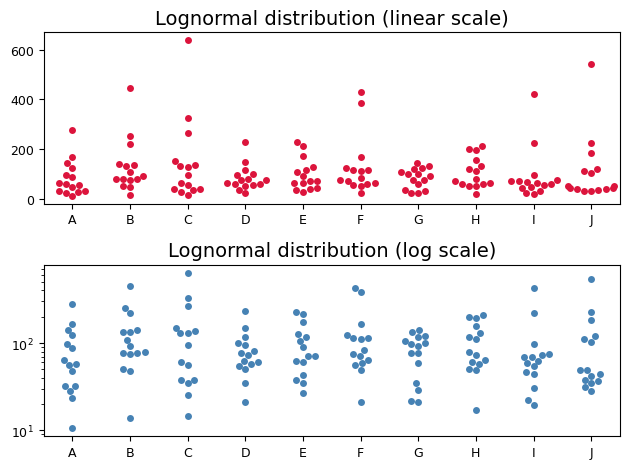

The case of log-normal data#

Sometimes, data doesn’t fit the familiar bell-shaped curve of a normal distribution. One common scenario is log-normal data, where the logarithms of the values follow a normal distribution. This type of distribution often arises in situations where the data represents multiplicative processes or where the values are inherently positive and skewed to the right. This skew can create a misleading impression of outliers when viewed on a linear scale.

To illustrate the characteristics of log-normal data and the potential misidentification of outliers, consider the following example. We’ve generated 10 random samples (labeled A-J), each containing 15 values drawn from the same log-normal distribution.

np.random.seed(111) # for reproducibility

# Parameters

mean = np.log(80) # Mean of the underlying normal distribution

# (calculated from the desired median of the lognormal distribution)

sigma = 0.8 # Standard deviation of the underlying normal distribution

labels = list("ABCDEFGHIJ")

sample_size = 15

# Generate data

data = np.random.lognormal(

mean,

sigma,

size=(len(labels), sample_size)

)

# Flatten and create labels for seaborn

flattened_data = data.flatten()

sample_labels = np.repeat(labels, sample_size)

data_dict = {

'Sample': sample_labels,

'Value': flattened_data}

# Plotting

fig, axes = plt.subplots(nrows=2, ncols=1,)

# Plot 1: Linear Scale

sns.swarmplot(

x=np.tile(labels, sample_size),

y=data.flatten(),

color="crimson",

# size=4,

ax=axes[0],

)

axes[0].set_title(

"Lognormal distribution (linear scale)",)

# Plot 2: Log Scale

sns.swarmplot(

x=np.tile(labels, sample_size),

y=data.flatten(),

color="steelblue",

# size=4,

ax=axes[1],

)

axes[1].set_yscale("log")

axes[1].set_title("Lognormal distribution (log scale)",)

plt.tight_layout();

The top swarm plot shows the raw, untransformed data. Notice the rightward skew, with most values clustered towards the lower end and a few extreme values stretching out the tail. On this linear scale, these extreme values might be mistakenly labeled as outliers.

However, the bottom swarm plot reveals a different story. Here, the y-axis is transformed to a logarithmic scale. The points now align more closely along a horizontal line, resembling the pattern expected from a normal distribution. This visual transformation confirms that the logarithms of the data are approximately normally distributed, a hallmark of log-normal data. Crucially, the values that appeared as outliers on the linear scale are now seen as part of the normal variation within the log-transformed distribution.

Understanding whether the data is log-normal has important implications for the analysis:

Transformation for normality: if we need to apply statistical methods that assume normality, we might be able to transform log-normal data into a normal distribution by taking the logarithm of each value. This can open up a wider range of analysis techniques.

Interpreting descriptive statistics: for log-normal data, the geometric mean is often a more appropriate measure of central tendency than the arithmetic mean, which can be heavily influenced by extreme values.

Modeling: log-normal distributions are frequently used to model phenomena like income distribution, stock prices, and biological growth processes.

Avoiding misinterpretation of outliers: as demonstrated in the plots, careful consideration of the appropriate scale is crucial when identifying outliers in log-normal data. Blindly applying outlier detection methods on the raw data can lead to erroneous conclusions.

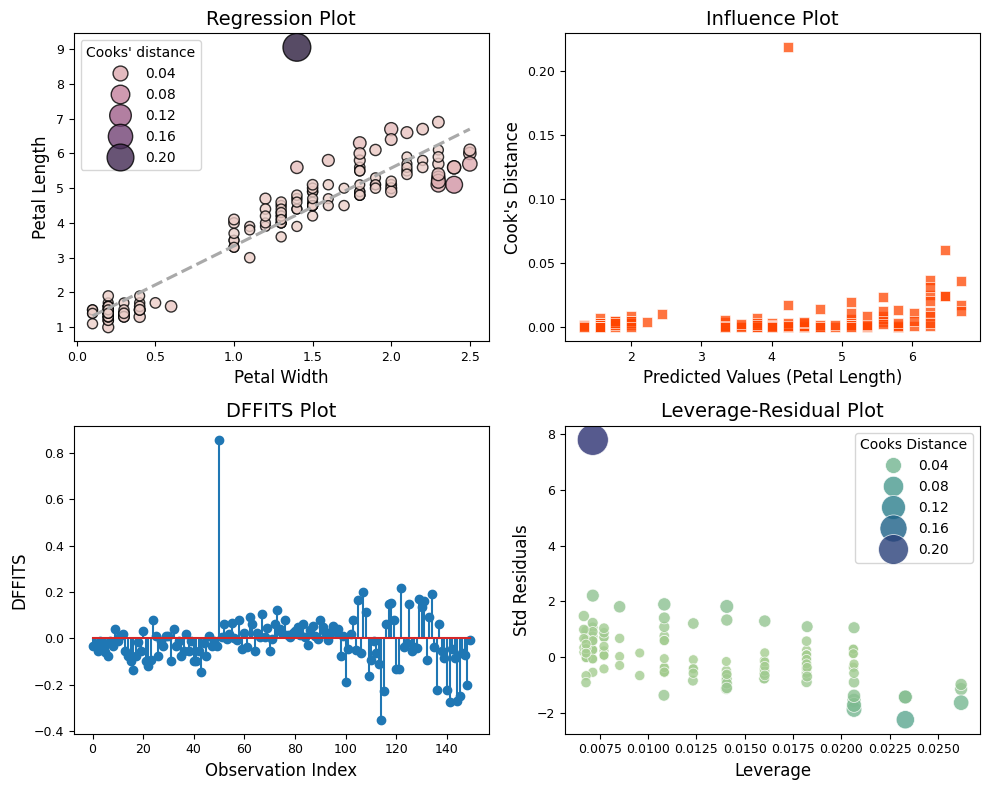

Cook’s distance and leverage#

Cook’s distance is a statistical measure of the influence of a data point on a regression model, i.e., it is not applicable to general outlier detection in other types of data without a regression context. It’s not a visual test in itself, but it can be used to inform visual inspection. Cook’s distance is calculated based on the residuals (the differences between the observed and predicted values) and the leverage (how far the predictor values are from their mean) of each data point in a regression model. Of note, a high leverage point can have a high Cook’s distance even if its residual isn’t that large. Higher Cook’s distance values indicate that a data point has a greater influence on the model’s fitted values.

We can plot Cook’s distances against data point indices or predictor values to visually identify highly influential data points that significantly modify the regression coefficients. For example, we can leverageg the statsmodels.stats.outliers_influence.OLSInfluence class to calculate outlier and influence measures on the R iris dataset. While often used for classification, e.g., for machine learning, the iris dataset includes continuous variables like sepal length and width that we can use for regression analysis.

# load the dataset

iris = sm.datasets.get_rdataset("iris").data

# rename columns to avoid PatsyError

iris.columns = iris.columns.str.replace(".", "_")

# create one exagerated outlier

iris.loc[50, 'Petal_Length'] = (

iris['Petal_Length'].mean() + 3 * iris['Petal_Length'].std()

)

iris.info()

<class 'pandas.core.frame.DataFrame'>

RangeIndex: 150 entries, 0 to 149

Data columns (total 5 columns):

# Column Non-Null Count Dtype

--- ------ -------------- -----

0 Sepal_Length 150 non-null float64

1 Sepal_Width 150 non-null float64

2 Petal_Length 150 non-null float64

3 Petal_Width 150 non-null float64

4 Species 150 non-null object

dtypes: float64(4), object(1)

memory usage: 6.0+ KB

import pandas as pd

from statsmodels.formula.api import ols

from statsmodels.stats.outliers_influence import OLSInfluence

# fit the regression model using statsmodels library

model = ols(

formula="Petal_Length ~ Petal_Width",

data=iris

).fit()

# Calculate Cooks' distance, leverage, DFFITS, and standardized residuals

influence = OLSInfluence(model)

cooks_distance = influence.cooks_distance[0]

leverage = influence.hat_matrix_diag

dffits = influence.dffits[0]

standardized_residuals = influence.resid_studentized_internal

predicted_values = model.fittedvalues

# Set font sizes for title and labels before creating the plot

title_fontsize = 14

label_fontsize = 12

ticks_fontsize = 9

plt.rcParams.update({

'axes.titlesize': title_fontsize,

'axes.labelsize': label_fontsize,

'xtick.labelsize': ticks_fontsize,

'ytick.labelsize': ticks_fontsize,

})

# Create a figure with four subplots sharing a y-axis

fig, axes = plt.subplots(nrows=2, ncols=2, figsize=(10, 8))

# Subplot 1: Regression Plot

sns.scatterplot(

x='Petal_Width',

y='Petal_Length',

data=iris,

hue=cooks_distance,

size=cooks_distance,

sizes=(50, 400),

alpha=.8,

edgecolor='black',

linewidth=1,

ax=axes[0, 0],

)

sns.regplot(

x='Petal_Width',

y='Petal_Length',

data=iris,

scatter=False,

ax=axes[0, 0],

ci=False,

line_kws={'color': 'darkgrey', 'ls': '--'}

)

axes[0, 0].set_xlabel("Petal Width")

axes[0, 0].set_ylabel("Petal Length")

axes[0, 0].set_title('Regression Plot')

axes[0, 0].legend(title="Cooks' distance")

# Subplot 2: Cooks' distance vs. Predicted Values

sns.scatterplot(

x=predicted_values,

y=cooks_distance,

color='orangered',

ax=axes[0, 1],

s=50,

marker='s',

alpha=.75,

)

axes[0, 1].set_title("Influence Plot")

axes[0, 1].set_xlabel("Predicted Values (Petal Length)")

axes[0, 1].set_ylabel("Cook's Distance")

# Subplot 3: DFFITS Plot

axes[1, 0].stem(dffits)

axes[1, 0].set_title('DFFITS Plot')

axes[1, 0].set_xlabel('Observation Index')

axes[1, 0].set_ylabel('DFFITS')

# Subplot 4: Influence Plot (Bubble Plot)

influence_data = pd.DataFrame({

'Leverage': leverage,

'Std Residuals': standardized_residuals,

'Cooks Distance': cooks_distance,

})

sns.scatterplot(

x='Leverage',

y='Std Residuals',

data=influence_data,

size='Cooks Distance',

sizes=(50, 500),

alpha=.8,

hue='Cooks Distance',

palette='crest',

ax=axes[1,1],

)

axes[1, 1].set_title('Leverage-Residual Plot')

# Display all plots

plt.tight_layout();

The four plots - regression with Cook’s distance as hue, Cook’s distance vs. predicted values, DFFITS plot, and leverage-residual plot - offer complementary perspectives on the impact of the outlier in the regression analysis.

Regression Plot with Cook’s Distance as Hue

The outlier is immediately noticeable due to its distinct color, indicating a high Cook’s distance.

Visually, we can see how the outlier pulls the regression line towards itself, demonstrating its disproportionate influence on the fitted values.

Cook’s Distance vs. Predicted Values

The outlier stands out with a much higher Cook’s distance than other points.

Its position on the x-axis (predicted values) might give clues about its nature. For instance, if it’s far from the other predicted values, it suggests that the outlier is not only influential but also poorly predicted by the model.

DFFITS Plot

The outlier is likely the point with the highest absolute DFFITS value, indicating that its removal would lead to a substantial change in its own predicted value.

This plot confirms the outlier’s influence on the model’s predictions.

Leverage-Residual Plot (Influence Plot)

The outlier appears in the upper right or lower right quadrant, indicating high leverage and a large residual.

This plot highlights how the outlier is both unusual in its predictor values (leverage) and has a large discrepancy between its observed and predicted values (residual), making it a particularly influential point.

The consistent identification of the outlier across all four plots underscores its strong influence on the regression model. This outlier is not merely an extreme value but also exerts significant leverage, affecting both the overall fit of the model and individual predictions.

There’s no strict cutoff for what constitutes a “high” Cook’s distance. It depends on the sample size and the specific context of the analysis. A common rule of thumb is to investigate points with a Cook’s distance greater than \(4/n\) (where \(n\) is the sample size), but it’s also essential to examine the plot visually to identify any points that stand out from the rest, regardless of the numerical threshold.

Some statisticians suggest investigating data points with a Cook’s distance greater than 1 divided by the square root of the sample size (\(1/\sqrt{n}\)). This threshold is generally more conservative than the \(4/n\) rule and might be more appropriate for smaller sample sizes. In another rule, the threshold is \(2 \times \sqrt{(p+1)/n}\), with \(p\) the number of predictor variables on the regression model. Neither rule is a definitive cut-off. They are meant as guidelines to help us identify points that warrant further investigation.

Statistical outlier detection#

Grubbs’ test#

While visual inspection provides a valuable first look, statistical tests offer a more objective way to identify outliers. One such test, well-suited for detecting a single outlier in a normally distributed dataset, is Grubbs’ test.

Grubbs’ test calculates a test statistic (\(G\)) that quantifies how many standard deviations the most extreme value in the dataset is from the sample mean. While similar in concept to z-scores and t-statistics, Grubbs’ test statistic uses a specific distribution (the studentized maximum modulus distribution) to determine its critical values and p-values. It’s worth noting that the term “extreme studentized deviate (ESD) test” is sometimes used interchangeably with Grubbs’ test, particularly when testing for multiple outliers.

Null hypothesis: the null hypothesis (H0) states that there are no outliers in the data.

Test statistic: Grubbs’ test calculates a test statistic (\(G\)) based on the maximum deviation of the data point from the sample mean, divided by the sample standard deviation (\(G = \max_{i} \left|\frac{y_{i} − \bar{y}}{s}\right|\)).

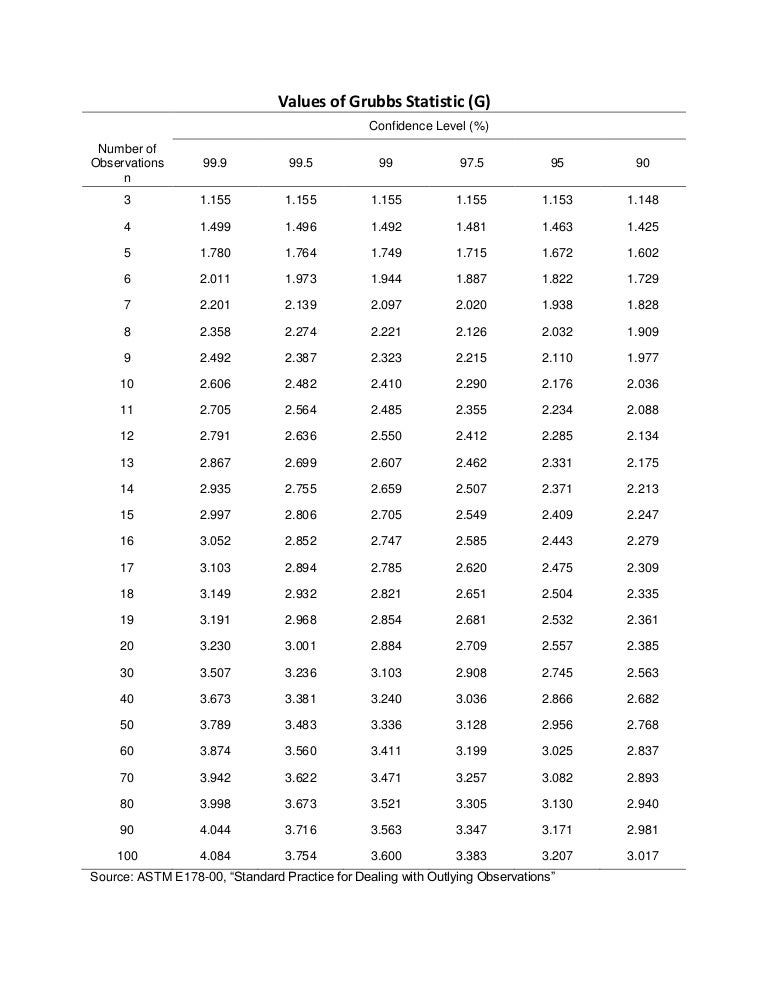

Critical value: this test statistic is compared to a critical value that depends on the desired significance level (e.g., 0.05) and the sample size. For example the critical G values for one-sided test can be found in the table below:

Decision:

If the test statistic is greater than the critical value, we reject the null hypothesis and conclude that the most extreme value is a significant outlier.

If the test statistic is less than or equal to the critical value, we fail to reject the null hypothesis, suggesting that the extreme value may not be a true outlier.

Let’s put Grubbs’ test to work on a concrete example. We generate data from a normal distribution, intentionally introduce an exaggerated outlier, and then calculate the Grubbs’ statistic to see if the test can successfully detect it.

def grubbs_gmax(n, alpha=0.05, onesided=False):

"""

Critical value for Grubbs' test for outlier.

>>> grubbs_gmax(n=8, alpha=0.05, onesided=False)

2.126645087195626

>>> grubbs_gmax(n=8, alpha=0.05, onesided=True)

2.031652001549952

See also:

https://ycopin.pages.in2p3.fr/Informatique-Python/Annales/22-grubbs/exam22_corrige.html

"""

sl = alpha / n # one-sided

if not onesided: # two-sided

sl /= 2

# Critical value (squared) of the t distribution w/ n-2 DoF and

# significance level sl

cv2 = st.t.isf(sl, n - 2) ** 2

gmax = (n - 1) * np.sqrt(cv2 / (n - 2 + cv2) / n)

return gmax

# Generate normal sample with an outlier

np.random.seed(123) # For reproducibility

sample_size = 100

sample = np.random.normal(0, 1, sample_size)

sample[0] = 5 # Introduce an exaggerated outlier

# Grubbs' Test (Manual Implementation)

def grubbs_test_manual(data, alpha=0.05):

"""Performs a two-sided Grubbs' test manually."""

sample_mean = np.mean(data)

sample_std = np.std(data, ddof=1) # Use ddof=1 for sample standard deviation

# Calculate G statistic (using absolute value for two-sided test)

G = np.max(np.abs(data - sample_mean)) / sample_std

# Critical value from Grubbs' table or using t-distribution

G_critical = grubbs_gmax(n=len(data), alpha=alpha, onesided=False)

return G, G_critical

# Perform manual Grubbs' test

G_calculated, G_critical = grubbs_test_manual(sample)

print("\n--- Manual Grubbs' Test ---")

print(f"Test Statistic (G): {G_calculated:.3f}")

print(f"Critical Value (G): {G_critical:.3f}")

if G_calculated > G_critical:

print("Reject H0: Evidence suggests the presence of a significant outlier.")

else:

print("Fail to reject H0: Insufficient evidence to conclude there is an outlier.")

--- Manual Grubbs' Test ---

Test Statistic (G): 3.985

Critical Value (G): 3.384

Reject H0: Evidence suggests the presence of a significant outlier.

Additional statistical methods for outlier detection#

There are several other statistical methods to identify outliers, each with its own strengths and weaknesses depending on the data and assumptions.

Generalized Extreme Studentized Deviate (GESD) Test: this test extends Grubbs’ test to detect multiple outliers in a normally distributed dataset. It’s implemented in the

outlierslibrary.Dixon’s Q Test: another test for outliers, but it’s more sensitive to outliers at the ends of the distribution and can be less powerful for outliers near the center. Sebastian Raschka has implemented the Dixon’s Q test elsewhere.

T-test based Outlier Detection: we can perform t-tests comparing each data point against the mean of the remaining data to identify outliers. This can be computationally intensive for large datasets.

sklearnprovides different unsupervised outlier detection algorithms:Fitting an elliptic envelope: fits a robust covariance estimate to the data, and thus fits an ellipse to the central data points, ignoring points outside the central mode.

Isolation Forest: isolates anomalies by randomly partitioning the data and measuring how easily a point can be isolated from others. Good for detecting outliers in both small and large datasets.

Local Outlier Factor (LOF): calculates a score for each point based on its local density compared to its neighbors. Points with significantly lower density than their neighbors are considered outliers.

One-Class SVM: learns a decision boundary around the “normal” data and classifies points outside this boundary as outliers. Useful when we have a good representation of the normal data but few examples of outliers.

Robust outlier detection based on the MAD-median rule as implemented in

pingouin.madmedianrule: the MAD-median-rule will refer to declaring \(X_{i}\) an outlier if \(\frac{\left | X_i - M \right |}{\text{MAD}_{\text{norm}}} > K\), where \(M\) is the median of \(X\), \(\text{MAD}_{\text{norm}}\) the normalized median absolute deviation of \(X\), and \(K\) is the square root of the 0.975 quantile of a \(\chi^2\) distribution with one degree of freedom (which is roughly equal to 2.24).

# Returns a boolean array indicating whether each sample

# is an outlier (True) or not (False)

pg.madmedianrule(sample)

array([ True, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False, False, False, False, False, False, False, False, False,

False])

The choice of outlier detection method depends on various factors:

Number of outliers expected: Grubbs’ test is for single outliers, GESD test for multiple.

Distribution of the data: Grubbs’ and GESD assume normality. Non-parametric methods like Isolation Forest are more flexible.

Data type: some methods are better suited for univariate data, while others can handle multivariate data.

Conclusion#

In this chapter, we’ve embarked on a journey to understand the critical role of normality assumptions in statistical analysis. We’ve explored a toolkit of graphical methods (like Q-Q plots) and statistical tests (such as the Shapiro-Wilk and D’Agostino-Pearson tests) for assessing whether our data conforms to the familiar bell curve. We’ve delved into the nuances of skewness and kurtosis, those telltale signs of departure from normality, and discovered how to leverage different Python packages for efficient testing.

We then ventured into the realm of outliers, those unexpected data points that can wreak havoc on our analyses if left unchecked. We learned how to visually identify outliers using various plots and then put them to the test using Grubbs’ test and the powerful arsenal of outlier detection methods available in libraries like statsmodels, pingouin, and scikit-learn.

Armed with this knowledge, we’re now equipped to:

Critically assess the normality assumption: don’t blindly apply statistical tests that require normality. Instead, use the tools we’ve learned to rigorously evaluate whether the data meets this crucial assumption.

Choose the right test: understand the strengths and limitations of different normality tests and select the one best suited for the specific data and research question.

Identify and handle outliers: detect outliers using a combination of visual inspection and statistical tests, and make informed decisions about how to handle them in the analysis.

Explore further: this chapter has only scratched the surface of normality testing and outlier detection. There’s a wealth of additional methods and techniques to explore. Consider delving deeper into robust statistics, nonparametric methods, and specialized techniques for multivariate data.

Normality and outliers are not mere theoretical concepts but practical considerations that can significantly impact the validity and reliability of our statistical findings. By mastering these tools and approaches, we’ll be well on our way to becoming a more discerning and confident data analyst!

Cheat sheet#

This cheat sheet provides a quick reference for essential code snippets used in this chapter.

Q-Q plots#

import numpy as np

import matplotlib.pyplot as plt

# Toy sample

np.random.seed(111)

data = np.random.normal(size=100)

# Q-Q plot with SciPy

from scipy.stats import probplot

# Generate the plot

ax = plt.subplot(111) # mandatory for probplot

probplot(data, plot=ax)

# Q-Q plot with Pingouin

import pingouin as pg

pg.qqplot(

data,

dist='norm', # compare data against the normal distribution

confidence=0.95, # add 95% confidence intervals

)

Statistical tests for normality#

# Skewness and Kurtosis

from scipy.stats import skew, kurtosis, describe

skew(data)

kurtosis(data)

describe(data) # detailed statistics incl. Skew and Kurtosis

# K² test

from scipy.stats import normaltest

normaltest(data) # returns k2, pval

# Shapiro-Wilk test

from scipy.stats import shapiro

shapiro(data) # returns W, pval

# Omnibus test

import statsmodels.api as sm

sm.stats.stattools.omni_normtest(data)

# Normality tests with Pingouin

import pingouin as pg

pg.normality(

data,

method='shapiro', # options are ['shapiro', 'normaltest', 'jarque_bera']

)

# Nonparametric Kolmogorov-Smirnov test

from scipy.stats import kstest

kstest(

data,

'norm',

)

Outliers#

# Cook's distance and leverage

from statsmodels.formula.api import ols

from statsmodels.stats.outliers_influence import OLSInfluence

# load the dataset

iris = sm.datasets.get_rdataset("iris").data

iris.columns = iris.columns.str.replace(".", "_")

# create one exagerated outlier

iris.loc[50, 'Petal_Length'] = (

iris['Petal_Length'].mean() + 3 * iris['Petal_Length'].std()

)

# fit the regression model using statsmodels library

model = ols(

formula="Petal_Length ~ Petal_Width",

data=iris

).fit()

# Calculate Cooks' distance, leverage, DFFITS, and standardized residuals

influence = OLSInfluence(model)

cooks_distance = influence.cooks_distance[0]

dffits = influence.dffits[0]

# Regression Plot

import seaborn as sns

sns.scatterplot(

x='Petal_Width',

y='Petal_Length',

data=iris,

hue=cooks_distance,

size=cooks_distance,

)

# DFFITS Plot

plt.stem(dffits)

# Robust outlier detection based on the MAD-median rule

pg.madmedianrule(iris['Petal_Length']) # returns array of True and False whether of not sample is outlier

Session Information#

The output below details all packages and version necessary to reproduce the results in this report.

Show code cell source

!python --version

print("-------------")

# List of packages we want to check the version

packages = ['numpy', 'scipy', 'statsmodels', 'pingouin', 'matplotlib', 'seaborn']

# Initialize an empty list to store the versions

versions = []

# Loop over the packages

for package in packages:

# Get the version of the package

output = !pip show {package} | findstr "Version"

# If the output is not empty, get the version

if output:

version = output[0].split()[-1]

else:

version = 'Not installed'

# Append the version to the list

versions.append(version)

# Print the versions

for package, version in zip(packages, versions):

print(f'{package}: {version}')

Python 3.12.4

-------------

numpy: 1.26.4

scipy: 1.13.1

statsmodels: 0.14.2

pingouin: 0.5.4

matplotlib: 3.9.0

seaborn: 0.13.2